Gas market overview Q4 2024

Volatility and Price Gains Close Out 2024

- Q3 Price Rally Sets Stage for an Even Stronger Q4

- Fastest Storage Depletion Since the Energy Crisis

- Europe Competes with Asia for LNG

Q3 Price Rally Sets Stage for an Even Stronger Q4

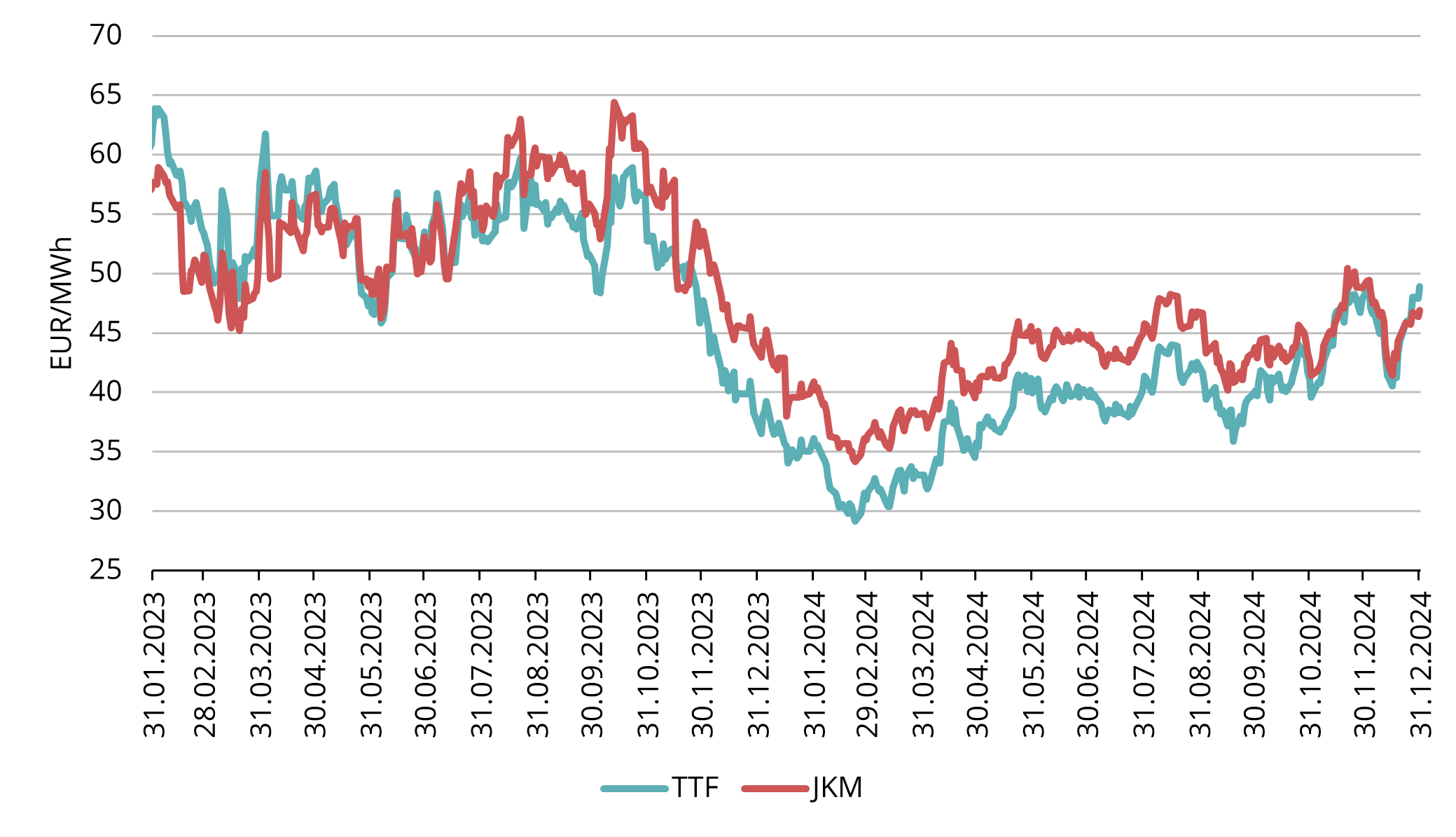

Figure 1. Gas prices, Refinitiv

After a steep decline in prices from late 2023 through Q1 2024, European natural gas markets rebounded sharply in Q2 and continued to climb through the rest of the year. The momentum from Q3 extended into Q4, culminating in the ICE TTF Front-Month futures surpassing €50/MWh on December 31, peaking at €50.57/MWh (see Fig. 1).

This quarter was marked by heightened uncertainty over Russian gas supplies to Europe. Speculation swirled around whether the gas transit through Ukraine would continue. Regular statements from political leaders stoked volatility, but ultimately, the transit agreement expired at year-end. With Russian pipeline gas last year representing only around 5% of Europe’s total supply, the gap will be filled by increased LNG imports.

Another significant development was the U.S. presidential election. Donald Trump’s victory signals a potentially favourable outlook for U.S. fossil fuel exports. While no immediate impact on global gas supply is expected—given the long lead times of LNG projects — this could further bolster U.S. LNG export capacity in the future, easing global supply constraints.

On the demand side, Europe experienced a sharp increase in gas consumption for power generation during Q4. While annual gas-to-power demand declined by 10% in 2024, thanks to growing renewable energy capacity and strong hydro reserves, Q4’s cold and windless conditions drove significant spikes. During November, gas consumption occasionally surged over 80% year-on-year (YoY). Overall, European gas demand in Q4 rose 9% YoY, according to the International Energy Agency (IEA).

The average Q4 price for the ICE Endex TTF front-month benchmark was €43.30/MWh, with forward contracts for February 2025 closing at €48.89/MWh on December 31 (see Fig. 1).

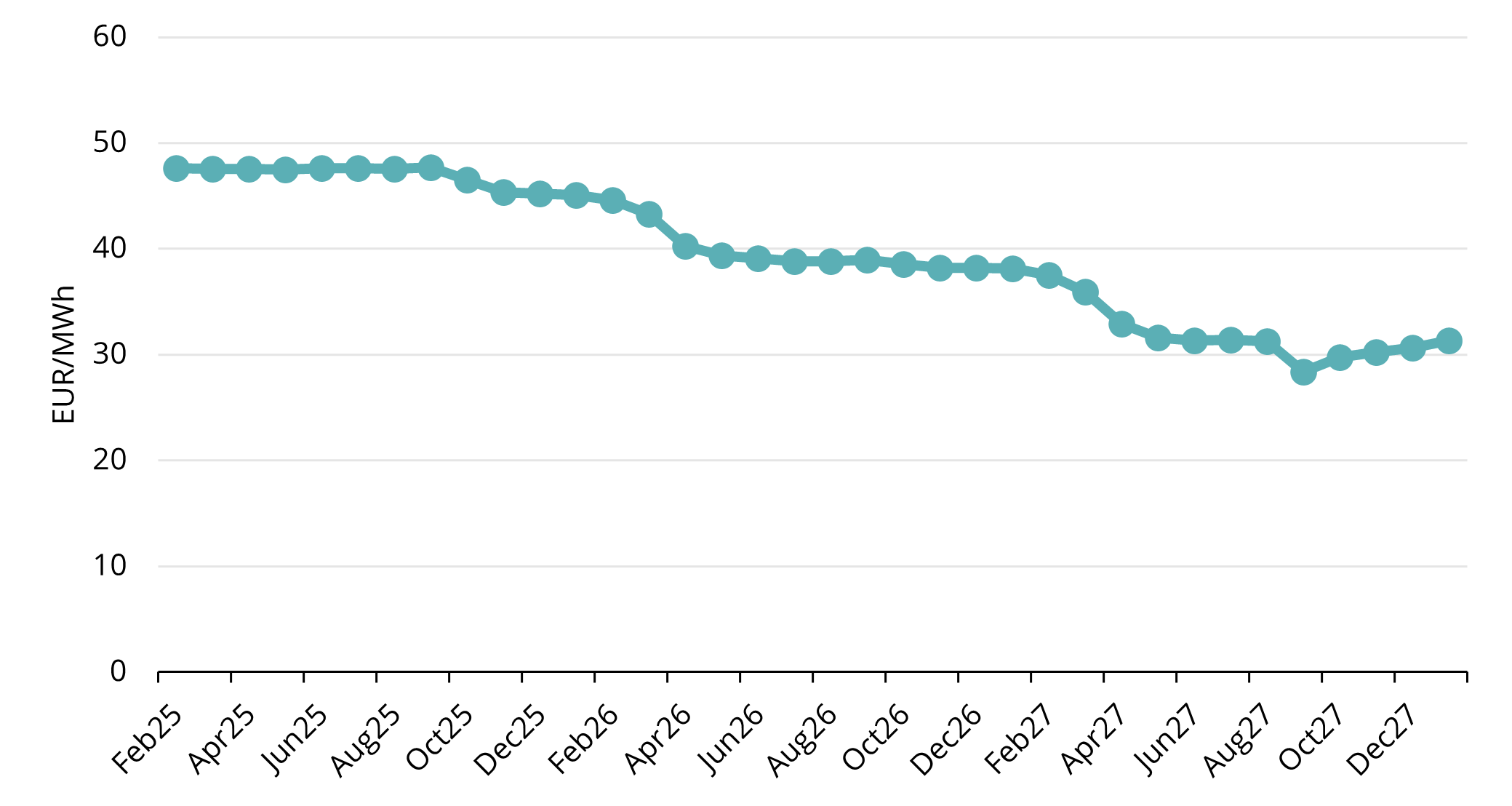

The forward curve for natural gas remains remarkably flat throughout the near months, with all contracts trading around 47-48 EUR/MWh until Sep-25 (see Fig. 2).

Figure 2. Natural Gas forward prices, Refinitiv

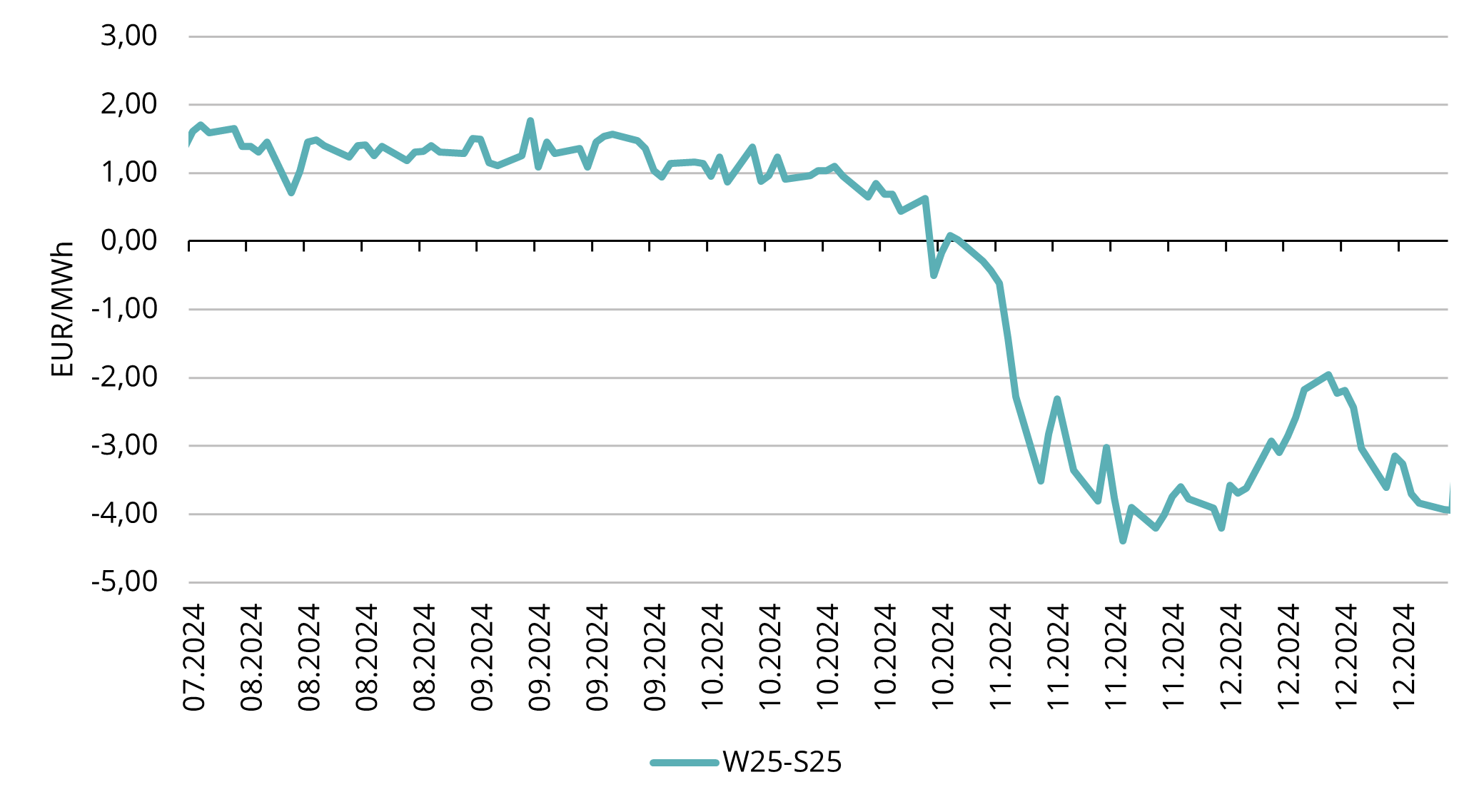

In a surprising twist, summer 2025 prices are trading higher than winter 2025 prices. This inversion defies conventional market logic, as storing cheaper summer gas for winter use is typically more economical. However, European regulations mandate that gas storages reach 90% capacity by November 1, forcing market participants to absorb summer injection losses to ensure security of supply for the Winter. LNG is not enough to cover the winter peaks. This naturally brings the question that why is the market in such a place?

The peculiar pricing reflects a combination of factors:

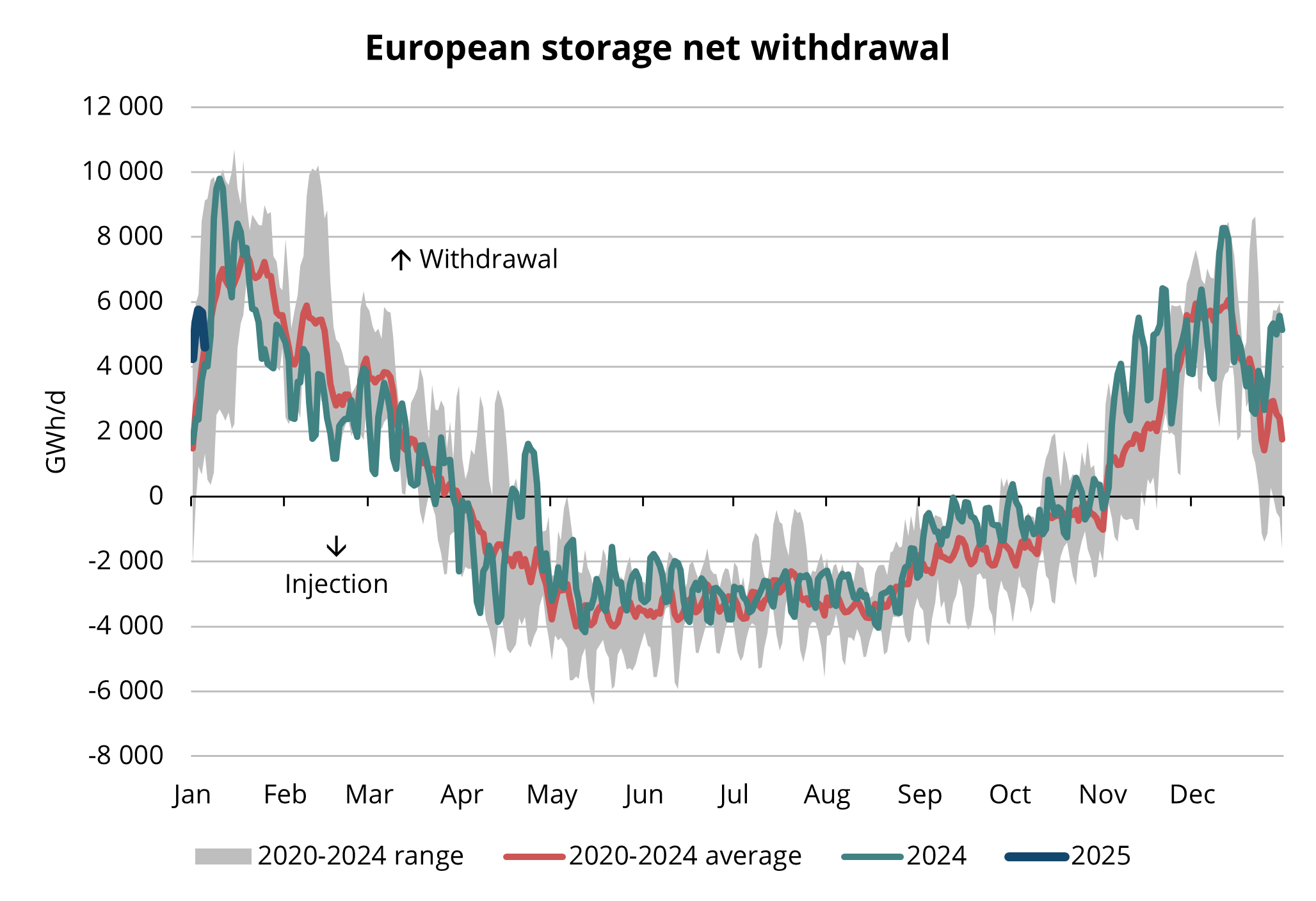

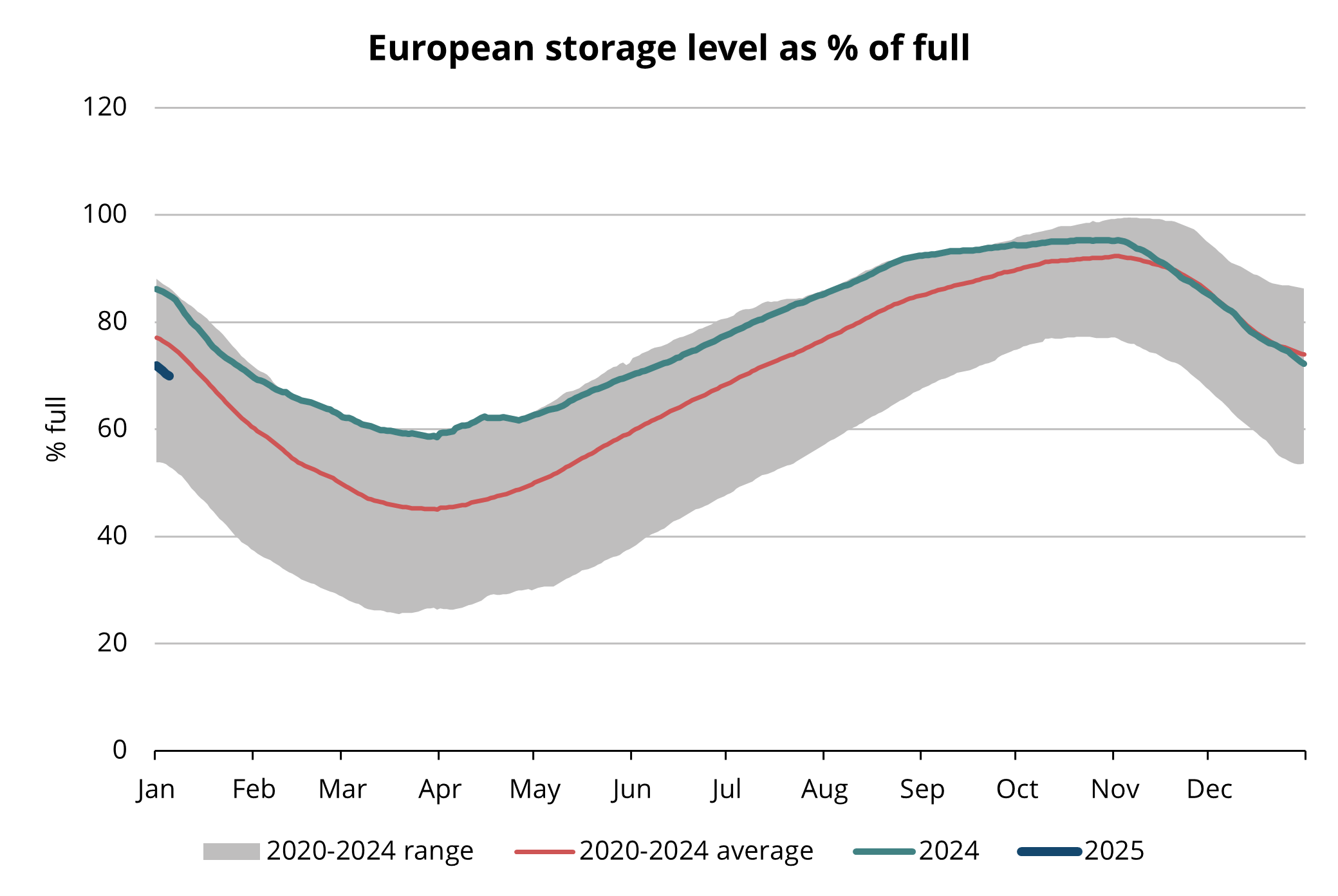

- Depleted Storage Levels: Heavy withdrawals in Q4 2024, driven by increased power generation demand, have brought European storage levels below the 5-year average (see Fig. 3 and 4).

- LNG Reliance: With no Russian pipeline flows expected in 2025, Europe must rely heavily on LNG imports to replenish stocks.

- Upcoming LNG Projects: New LNG facilities expected to come online in late 2024 and early 2025 would ease winter prices, but their impact on summer prices is more muted.

These dynamics make the summer-winter spread a crucial factor to watch in 2025, as regulatory mandates collide with market economics.

Figure 3. Seasonal injection and withdrawal at European storages, 2020-2025, AGSI+

Figure 4. Gas in European storage, 2020-2025, AGSI+

Fastest Storage Depletion Since the Energy Crisis

Europe entered the winter season with robust storage levels thanks to a mild 2023/24 winter. However, November and early December saw accelerated withdrawals as cold, windless weather boosted gas-for-power demand. By year-end, storage levels had fallen below the 5-year average (see fig.4), creating bullish momentum for prices.

The weather for the remainder of current winter is forecast to be rather mild, alleviating the pressure on storages somewhat. However, while current supplies remain sufficient for this winter, concerns are mounting over the coming summer. Analysts predict storage levels could fall to around 40% by spring 2025, compared to 55% the previous year. This creates greater summer demand to meet the EU’s 90% storage requirement by November.

The halt in Russian gas flows further complicates matters. Although these flows accounted for around 5% of European supply, their absence, combined with lower storage reserves, underscores Europe’s dependence on LNG. Fortunately, additional LNG capacity is expected to come online in Q4 2025 and Q1 2026, helping stabilize the market.

Figure 5. TTF Winter 2025 minus TTF Summer 2025 spread in EUR/MWh, Refinitiv

Hence, we are in a situation where as of 31.12.2024 the coming summer was around 4 EUR/MWh higher than the coming winter (see fig. 5).

The unusual summer-winter price spread has sparked debates about market stability and security of supply. With storage injections less economically viable, policymakers and market participants will closely monitor these trends in Q1 2025.

Europe Competes with Asia for LNG

The first months of 2025 will be pivotal in determining the trajectory of European gas prices. The level of gas in storage by the end of winter will dictate Europe’s LNG needs during the summer. LNG, a globally traded commodity, links European prices (TTF) with Asian benchmarks (JKM). In 2024, the two markets showed a strong price correlation of 0.95 (IEA) suggesting that they correlate almost perfectly. This means that Asian demand affects European prices a lot and vice versa.

Figure 6. LNG imports to Europe, Refinitiv

Looking at TTF and JKM spread (see fig. 1) we can see that at the end of Q3 TTF was trading around 2 EUR/MWh lower than JKM but in the end of Q4 TTF was already a more expensive hub than JKM. This spread is important because the more expensive hub is the one which attracts the spot LNG cargoes. Spot cargoes are fairly easy to divert for players between Europe and Asia and therefore the hub which currently needs more supply also has to pay more.

Current TTF levels are necessary for Europe to keep attracting LNG cargoes. From the fig. 1 we see that throughout the year JKM was more expensive than TTF and this affected Europe’s ability to attract the LNG. If we look at European LNG imports (see fig. 6) then they were clearly lower than the year before. One effect was that after the previous mild weather Europe needed less LNG to fill the storages, but the other factor was JKM-TTF spread and high Asian demand. As Q4 saw strong withdrawals in Europe then TTF price had to rise to attract LNG cargoes and bring in additional supply to Europe

Q4 2024 was marked by rising prices driven by geopolitical uncertainty, colder-than-expected weather, and increased power generation demand. For Q1 2025, weather patterns will play a critical role in shaping storage levels and summer LNG requirements. The evolving summer-winter spread and Europe’s competition with Asia for LNG will remain key themes in the year ahead.

This market overview is for informational purposes only. We aim to compile the most relevant data from various sources in good faith but the analysis should not be treated as an advice or taken as the sole basis for any action.