Gas market overview Q3 2025

Calm Quarter Amid Geopolitical Tensions

- Low Volatility During Q3

- Weaker Asian Demand Eased European Storage Concerns

- Baltic-Finnish Market Developments Strengthen Regional Integration

- Q4 Gas Market Outlook: Europe Ready for Winter, but Upside Risks Remain

Low Volatility During Q3

After a volatile spring, benchmark TTF month-ahead prices moderated in Q3, though they maintained a higher floor than pre-2022 structural norms. This reflects the ongoing premium for winter risk and the cost of competing for LNG cargoes.

The third quarter of 2025 saw a steady downward price trend: TTF front-month futures opened around €33.25/MWh on the first day of Q3 and closed below €31.50/MWh at the end of September.

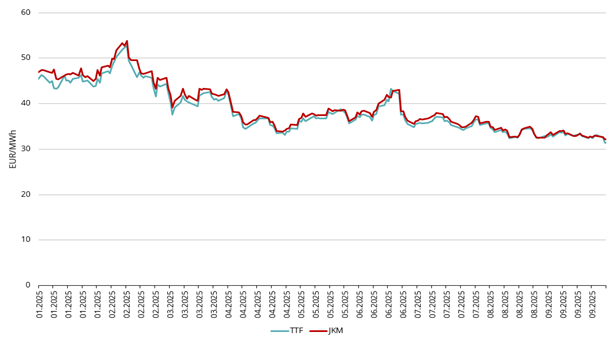

Figure 1. Gas prices, Refinitiv

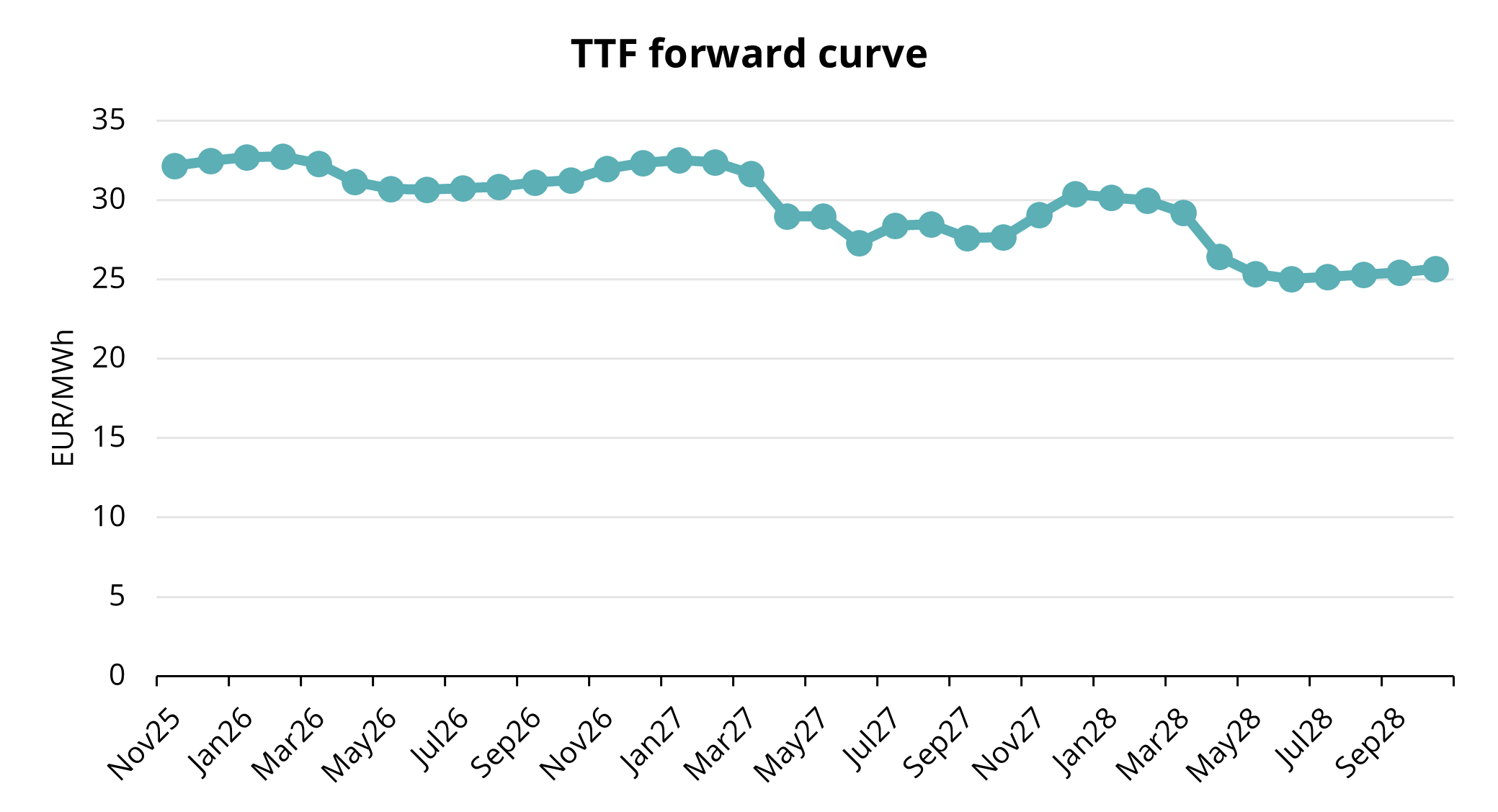

The average price for the ICE Endex TTF front-month benchmark during Q3-25 was 33.01 EUR/MWh, with forward contracts for the nearest full month, November 2025, closing at 31.41 EUR/MWh on September 30th (see Fig. 1). The forward curve for natural gas remains fairly flat throughout the near months, with coming Winter months trading around 33 EUR/MWh (see Fig. 2).

Figure 2. TTF forward prices, Refinitiv

One of the key milestones of Q3 was Canada’s launch of its first LNG exports from the Pacific Coast. This long-awaited project — the country’s first large-scale LNG export facility — establishes a new Pacific outlet for North American gas. The debut shipment shortens voyage times to Asia compared with U.S. Gulf Coast cargoes. While early volumes remain limited, commissioning strengthens supply diversity and is expected to ramp up through 2026. For Europe, the Canadian start-up is strategically relevant, contributing to the broader wave of North American supply growth expected to ease global tightness from mid-2026 onward.

At the same time, headlines emerged of a sanctioned Russian LNG cargo from Arctic LNG 2 delivered to Beihai, China. This illustrates how some Russian volumes continue to reach Asian buyers despite Western sanctions and logistical hurdles. These Arctic LNG 2 shipments to China persisted throughout Q3 and are likely to continue into Q4. Their redirection frees up additional U.S. and Atlantic Basin cargoes for Europe, although it also complicates transparency and traceability in global LNG trading.

In a landmark policy step, the European Union announced plans to ban Russian LNG imports starting in 2027. Although Russian pipeline deliveries have already collapsed since 2022, LNG imports had persisted in modest volumes. The ban is unlikely to trigger a major price spike, as global shipping capacity and replacement supply from the U.S., Qatar, Africa, and Canada are expected to be sufficient by 2027. In practice, the measure will reshape trade routes rather than reduce supply:

- Russian LNG displaced from Europe will increasingly flow to Asia, particularly China and India;

- This will free more U.S. and Atlantic Basin LNG to move toward Europe;

- Overall, the result will be a re-routing of global flows rather than a net volume loss.

Weaker Asian Demand Eased European Storage Concerns

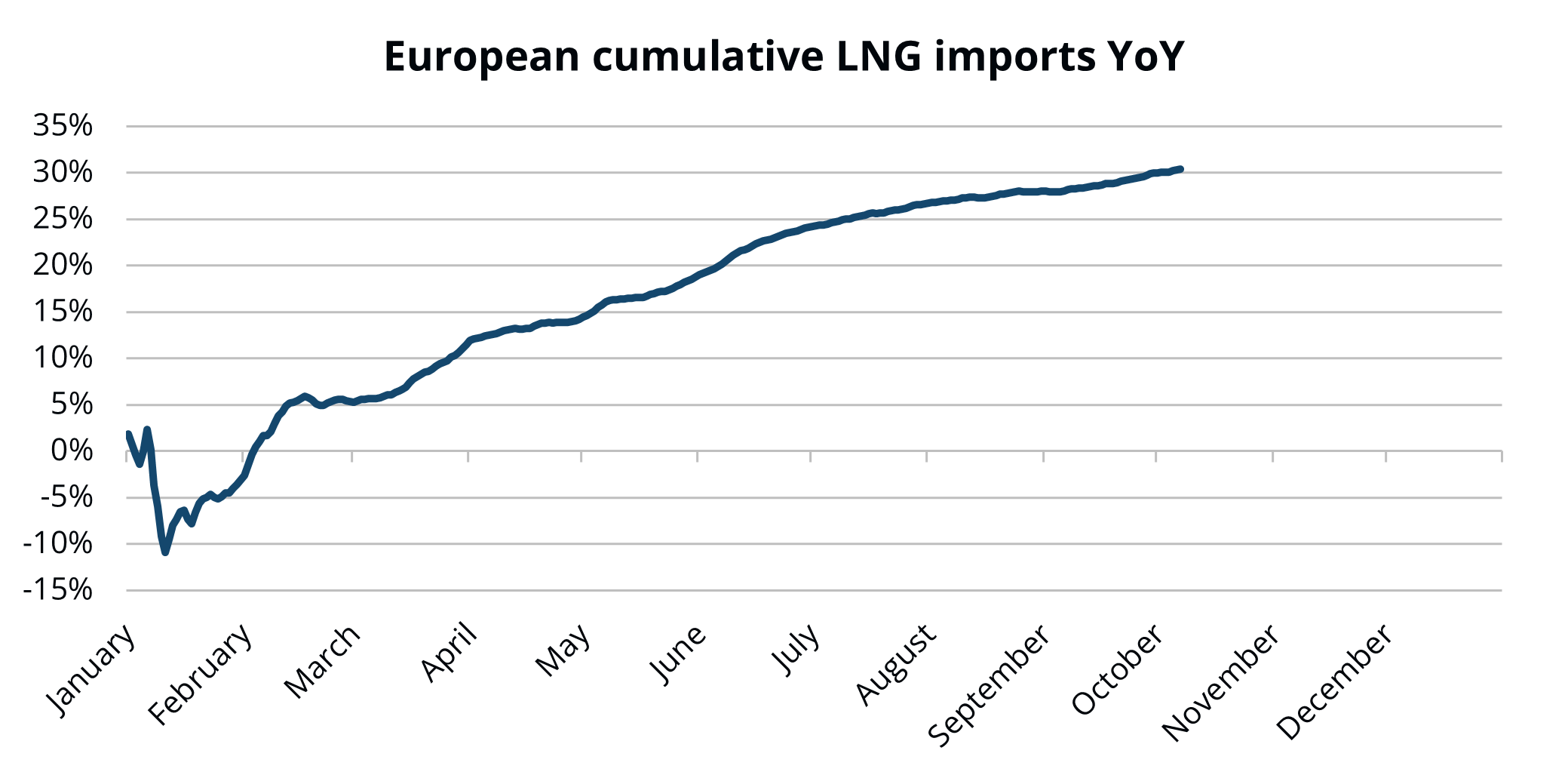

Figure 3. European cumulative LNG imports YoY, Refinitiv

Contrary to expectations, Asian LNG demand — particularly in China — remained subdued through Q3. China’s LNG imports fell sharply (by more than 20% year-on-year in many reports) as industrial activity weakened and gas substitution from domestic sources continued. Japan and Korea maintained stable import levels, but not enough to draw significant cargoes away from Europe.

With weaker competition from Asia, European LNG imports rose markedly versus the same period last year, supported by strong storage injection demand and dwindling pipeline alternatives. Spreads consistently favoured European landings over Asian diversions. By the end of Q3, Europe had imported nearly 30% more LNG over the first nine months of the year compared with 2024 (See Fig. 3).

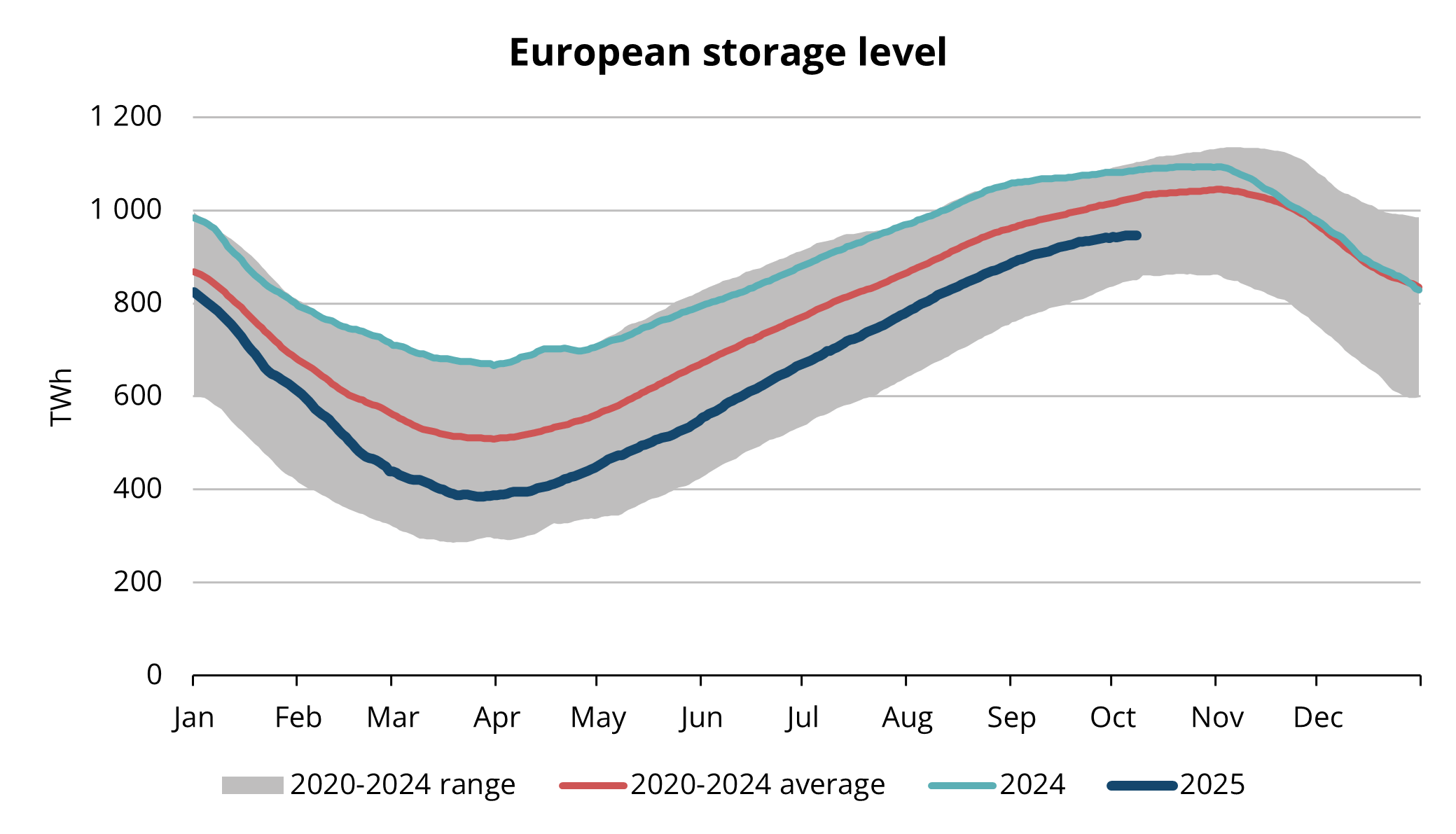

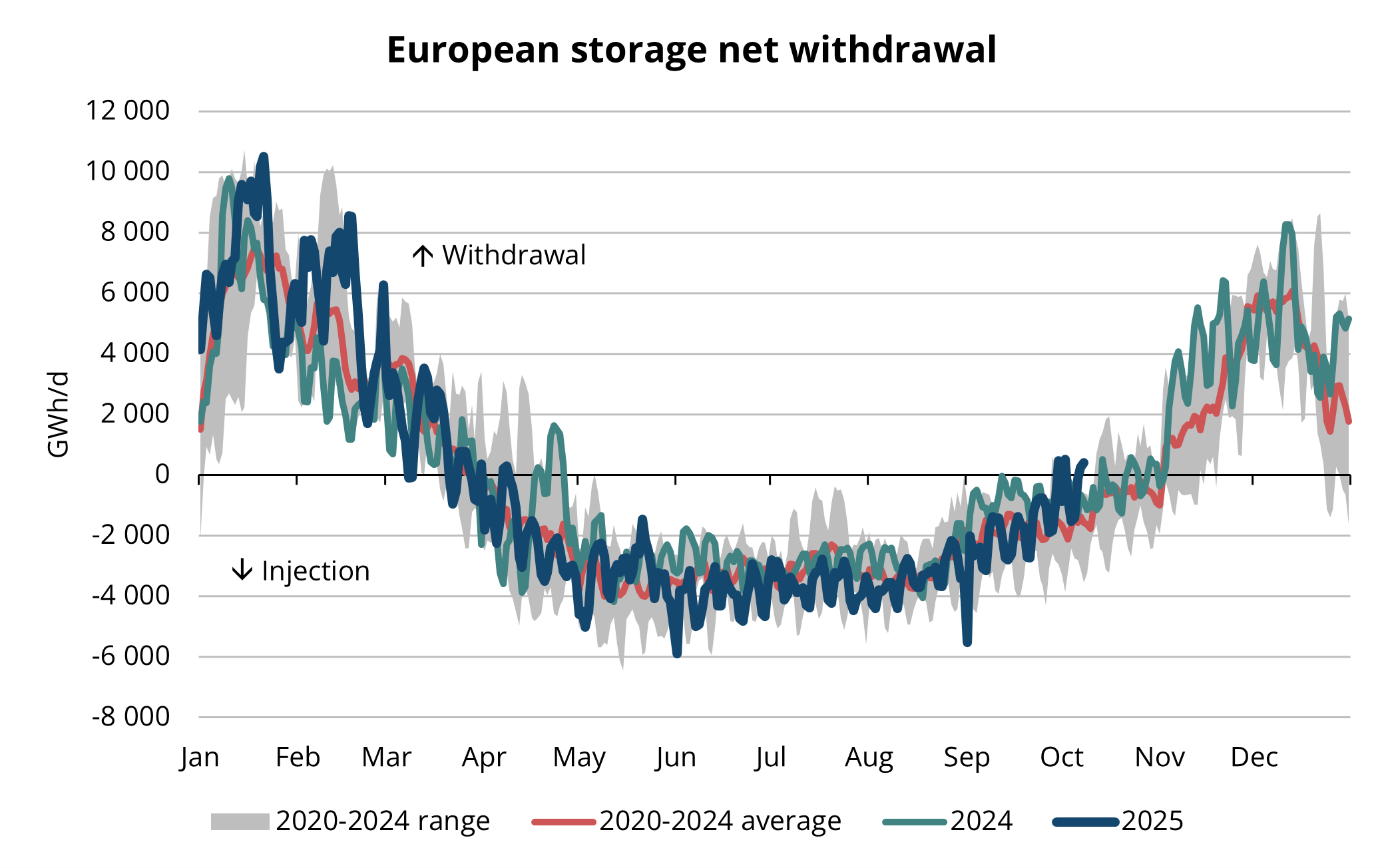

Europe needed every molecule of that LNG: the injection season began at significantly lower levels than in both 2024 and the five-year average. Robust LNG inflows enabled Europe to maintain high injection rates and enter autumn with stronger-than-expected storage levels, easing immediate market fears and capping potential price spikes. Nevertheless, storage is a buffer, not a substitute — its limits could be tested in the event of a prolonged cold spell or widespread infrastructure disruption during winter.

Figure 4. Gas in European storage, 2020-2025, AGSI+

Figure 5. Seasonal injection and withdrawal at European storages, 2020-2025, AGSI+

Baltic-Finnish Market Developments Strengthen Regional Integration

A significant step forward for regional market integration came in September, when the Baltic–Finnish gas market area was officially launched on the European Energy Exchange (EEX). This marks a shift from the previous GetBaltic platform toward a broader, EU-integrated framework. The EEX launch enhances transparency, liquidity, and cross-border efficiency, bringing the FinBalt region into closer alignment with continental European hubs. While trading volumes remain modest, participation is expected to grow as utilities and traders adapt to the new setup and leverage EEX’s hedging and clearing tools.

In another innovative development, Lithuania’s Klaipėda LNG terminal introduced a virtual biomethane liquefaction service. Under the scheme, biomethane injected into the grid can be certified and “linked” to LNG reloads, effectively allowing biomethane-backed LNG exports or bunkering. This enables reloaded LNG volumes to carry renewable origin guarantees — a first for the region — and opens an entirely new segment for “green LNG” trading. The system uses a book-and-claim model, ensuring traceable certification without requiring physical liquefaction. For Klaipėda, the innovation adds flexibility, strengthens its role as a regional hub for both natural and renewable gases, and aligns with EU goals for integrating renewable gases into the energy system.

Q4 Gas Market Outlook: Europe Ready for Winter, but Upside Risks Remain

As Europe heads into the heating season, weather remains the decisive factor for gas prices. Cold anomalies remain the single biggest wild card heading into Q4. A harsher-than-normal winter would push Europe to lean heavily into storage and LNG flexibility. Strong storage is a necessary safety barrier but not a guarantee. In a colder-than-expected Q4 or in the case of supply shocks, storage levels can be drawn down quickly. Moreover, withdrawal rates, bottlenecks in distribution, or infrastructure failures can stress the system even with decent inventories. In case of a cold winter many research houses see TTF prices shooting through 40 EUR/MWh. Conversely, a mild winter would relieve stress and allow a more balanced withdrawal profile and allow TTF prices to fall below 30 EUR/MWh.

On the LNG side, supply flexibility is tight heading into winter. Any maintenance delays, technical outages, or export curtailments (U.S., Qatar, Africa) will immediately tighten the market. Ambitious new liquefaction capacity slated for 2026 will start to ease constraints, but Q4 2025 will still operate under structural supply scarcity. If China or other Asian economies revive industrial activity and heating demand, some cargoes may divert from Europe. That scenario would reinstate more stress on Europe’s LNG sourcing. However, if Asia remains subdued, Europe enjoys a degree of relief — lower diversion risk and steadier access to LNG cargoes.

In today’s world there is also an ongoing geopolitics and infrastructure risks. New attacks or sabotages on pipelines, Russian attacks on Ukrainian gas infrastructure or Middle East tensions are all clear upside risk factors for gas prices. Military strikes and sabotage risks affect market sentiment even when physical flows are not immediately curtailed.

Despite the geopolitical uncertainty and potential winter volatility, Europe enters the cold season in a position of strength. Gas storages are well filled, LNG supply routes are diversified, and market integration continues to deepen.

This market overview is for informational purposes only. We aim to compile the most relevant data from various sources in good faith but the analysis should not be treated as an advice or taken as the sole basis for any action.