Gas market overview Q1 2025

Turning Point in European Gas Supply

- The End of Russian Pipeline Gas to Europe

- Storage Withdrawals at Four-Year High

- Europe Faces the Challenge of Filling the Storages

The End of Russian Pipeline Gas to Europe

Figure 1. Gas prices, Refinitiv

2025started off with a strong upward move in January on the back of the momentum from the end of 2024 culminating in the ICE TTF Front-Month futures reaching intraday high 59.39 EUR/MWh on Feb 11th and closing above 57 EUR/MWh (see Fig. 1).

Q1 2025 witnessed major transformations in the European gas market. The quarter was marked by the formal end of the Russian gas era in Europe, heightened policy debates, shifts in supply dynamics, and evolving energy security measures. Market participants navigated a complex interplay of regulatory changes, infrastructural challenges, and geopolitical maneuvers that are likely to influence the region’s gas landscape well into the future.

January and the first half of February saw a sharp rise in prices, driven by the effective end of Russian pipeline gas to Europe, cold and windless weather across the region, and concerns over European storage levels. In the second half of February, however, prices plummeted after the U.S. initiated peace negotiations with Ukraine and Russia.

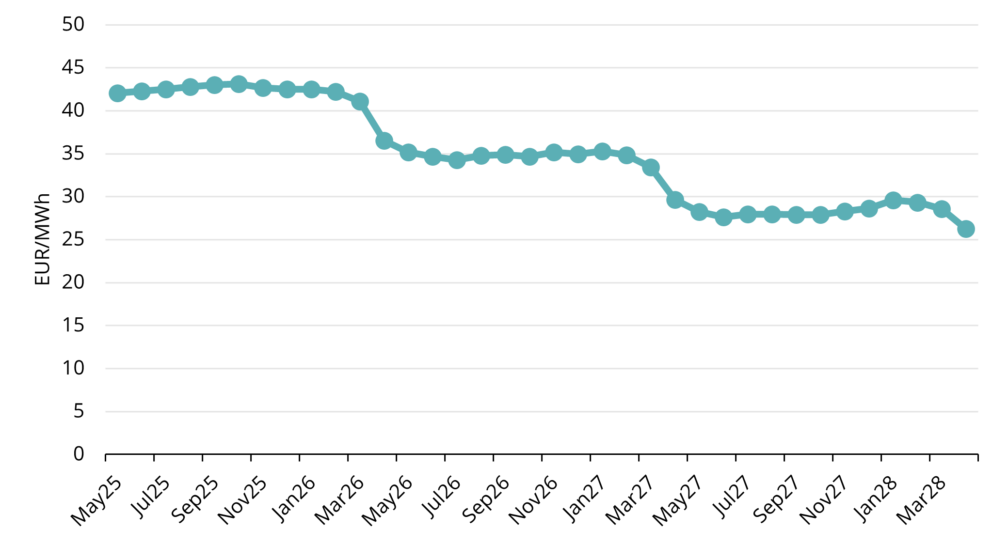

Figure 2. Natural Gas forward prices, Refinitiv

The average Q1 price for the ICE Endex TTF front-month benchmark was 46.762 EUR/MWh, with forward contracts for the nearest full month, May 2025, closing at 40.667 EUR/MWh on March 31st (see Fig. 1). The forward curve for natural gas remains remarkably flat throughout the near months, with all contracts trading around 42-43 EUR/MWh until Feb-26 (see Fig. 2).

Above means that winter gas prices are slightly higher than summer prices, making it economically unprofitable to inject gas during the summer and withdraw it in the winter — even before accounting for storage and financing costs. This has sparked an ongoing debate: Should Europe lower or even abolish its 90% November filling target, or should it remain in place? Many European countries have publicly expressed their view that storage regulations should be relaxed. So far, no decisions have been taken, but it is probable that Europe will relax interim targets for months before November but will keep in place the 90% target for the start of Winter.

Storage Withdrawals at Four-Year High

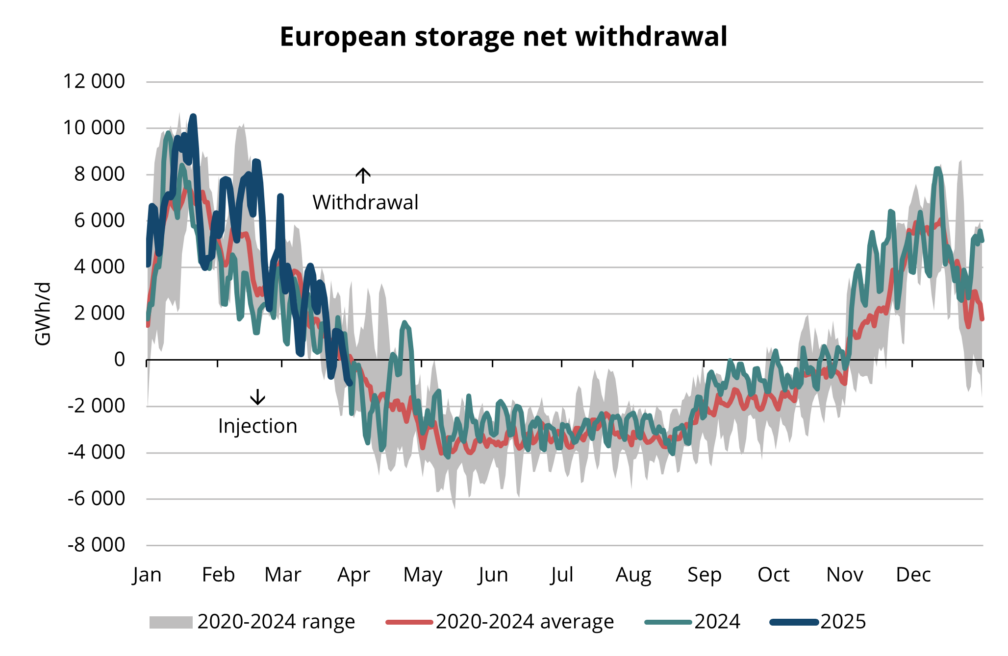

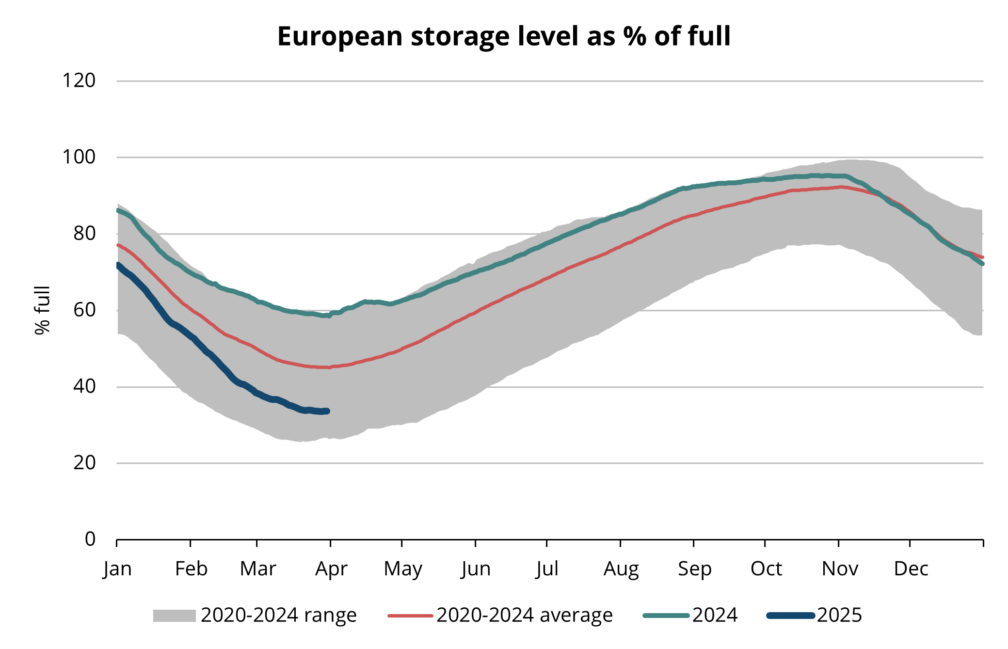

By the end of 2024 storage levels had already fallen below the 5-year average (see fig.3). January and the first half of February saw high depletion continuing as the weather across Europe was cold and windless which meant higher gas-to-power generation. After that the withdrawal levels fell back to the 2020-2024 range but were still higher compared to 2024 (see fig.4). In the end of March Europe saw first days of net injections, in line with historical behavior of the market.

As a result, at the end of March 2025 European storages stood close to 33% full, much lower than year before when the respective level was around 59% (see fig.4)

Figure 3. Seasonal injection and withdrawal at European storages, 2020-2025, AGSI+

Figure 4. Gas in European storage, 2020-2025, AGSI+

Europe Faces the Challenge of Filling the Storages

Storage levels around one third full mean that Europe has a wide gap to fill to achieve the storage targets and security of supply for next Winter season. Although at one point during March markets started to whisper about the possibility of Russian flows coming back to Europe as a part of a peace deal in the Russo-Ukrainian war then this likelihood seems close to zero as the end of quarter. Firstly, Nord Stream pipelines have not been usable for years and in March also the Sudzha pipeline, the one through which Russian gas got to Europe in 2024, was heavily hit and this means the infrastructure is not in place for return of Russian gas, despite any potential political agreement. This means Europe will need high LNG cargo arrivals and strong Norway pipeline flows throughout the Summer to refill the storages.

Summer ahead TTF is trading around 43 EUR/MWh, clearly higher compared to the 30-35 EUR/MWh average range during previous Summer. This reflects high demand and risks priced in during this Summer period. However, it also indicates that the market is in no panic mode as we are far away from any panic levels. The price of gas in Europe during the Summer, as well as the speed and final level of storage filling, depends primarily on three factors:

- Europe’s adjustments to storage targets – There is an ongoing debate about whether to modify interim targets and the final 90% storage level. Several European countries are advocating for more flexibility, but no definitive decision has been made yet. It is noteworthy that the 90% target could turn out to be unrealistic as for example, Wood Mackenzie’s base case for European storages are around 81% full.

- Norwegian gas flows and maintenance schedules – Summer is a peak maintenance period. Norway has forecasted higher pipeline gas deliveries to Europe compared to last Summer, but this depends on maintenance proceeding as planned. Any delays or unexpected issues in Norway’s maintenance schedules would put upward pressure on prices, given Norway’s significant role in Europe’s gas supply. However, if everything goes smoothly and the expected Norwegian flows materialize as planned, this could provide some relief for Summer gas prices.

- Asian demand – Europe competes with Asia for LNG, and cargoes are attracted to regions where prices are higher. At current price levels, Europe is considered a “premium market,” offering prices high enough to attract short-term LNG vessels. However, a very hot summer in Asia or faster-than-expected economic growth could drive up Asian gas consumption and prices, forcing European prices to rise to secure LNG supply. Conversely, if Asian demand is lower than expected competition in the LNG market would ease, bringing some relief to European prices.

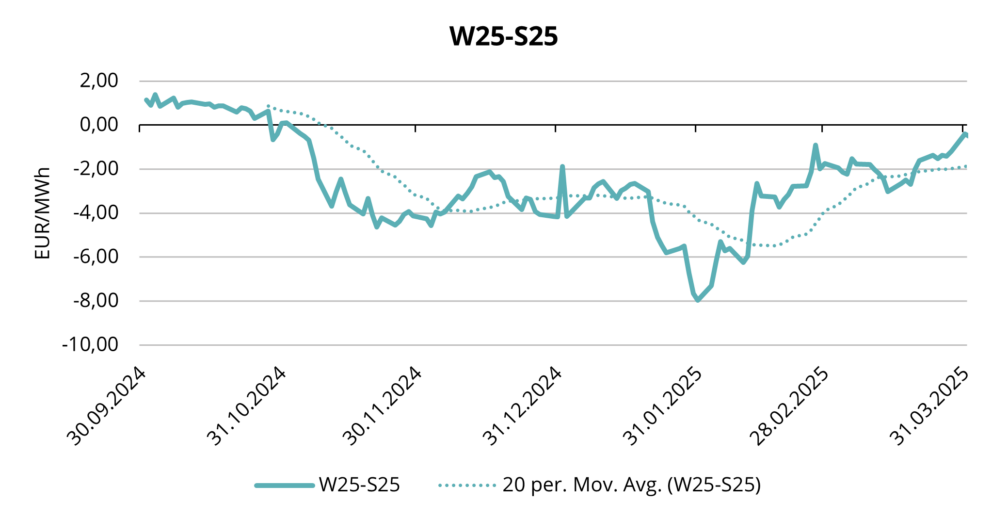

Figure 5. TTF Winter 2025 minus TTF Summer 2025 spread in EUR/MWh, Refinitiv

There lies one key problem in the market for Europe to fill its storage targets and this is Summer-Winter spread which is out-of-the-money, meaning that it is not economically feasible to inject gas into the storage and sell it in Winter. That is because even without storage and financing costs the pure TTF forward curve spread is not favorable – Winter prices are trading lower than Summer prices (see fig.5).

However, one can see from the graph above that although the spread still does not favor injections then it has become much more viable compared to February for example, where at one-point Summer prices were nearly 8 EUR/MWh higher than Winter prices. After the liquidation of big speculative positions, it has reached near flat levels. If everything goes as planned on the supply side, LNG cargoes keep heading towards Europe and Norway manages to fulfill its forecast and deliver larger pipeline volumes to Europe compared to Summer 2024, then it is very likely that this spread turns into positive, market players start injections and storage levels start to rise.

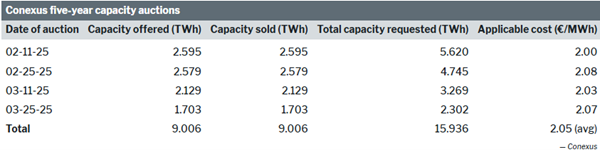

In Elenger’s home gas markets, the focus was primarily on Inčukalns storage auctions, as the Latvian storage site offered capacities for a five-year period for the first time ever. This represents a significant investment and decision for market participants. Given the current spreads on the curve, it is not economically viable, yet it remains crucial for ensuring energy security in the region. Four auction rounds were held, all of which were oversubscribed. In total, approximately 9 TWh of capacity was allocated at a weighted average price of 2.05 EUR/MWh (see Fig. 6), meaning that capacity holders must pay 2.05 EUR/MWh annually over the next five years for each MWh of allocated capacity.

Figure 6. Inculkans five-year capacity auctions, Conexus

Such oversubscription shows that the market is active and that the security of supply in the region is strong.

In conclusion, expected gas prices in Europe are set to be higher than last year due to a greater need for storage filling. In terms of supply security, Europe remains reliant on LNG cargoes and Norwegian pipeline gas flows. However, if everything proceeds as planned, Europe should be able to fill its storage without major issues. The key risk factors for European gas prices are potential disruptions in Norway’s maintenance schedule and fluctuations in Asian demand, coupled with unknown direction of European Union decisions regarding storage targets.

This market overview is for informational purposes only. We aim to compile the most relevant data from various sources in good faith but the analysis should not be treated as an advice or taken as the sole basis for any action.